Tuesday, May 26, 2015

Thursday, January 8, 2015

Well....your missing the boat on our amazing real estate market

You want to know one of the best investments going right now? Real estate in DFW. I sold a house to a sweet couple 1.5 years ago. We got them into the house for $330k. They have to sell their house today. I met with them to discuss market value. We can put that house on the market for $450 and probably sell in less than two weeks. That's quite an amazing return don't you think? Not only is it a great time to buy with the amazing interest rates, your ability to sell for a higher price and a faster timeframe is also quite strong. If you are looking at either buying or buying/selling, then you need to call me today. Not tomorrow! This real estate market is not going to last forever. Call me and I'll take good care of you! 214-837-0010

Thursday, October 23, 2014

Real Estate Home Prices Set To Continue Gains

How much gains? Your need to know real estate information http://www.dallasnews.com/business/residential-real-estate/20141016-tight-dallas-area-housing-market-will-continue-to-keep-prices-rising-sales-down.ece

Thursday, October 16, 2014

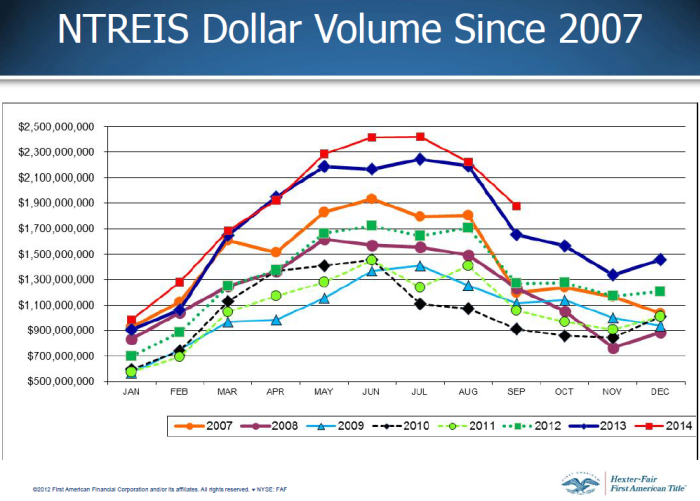

Dollar volume of home sales going back to 2007

Below is my latest update to the NETREIS Dollar Volume chart. As you can see, the dollar volume of single family home sales in the North Texas MLS system fell to $1.873 billion this month. Declines in dollar volume are certainly expected in September as many people try to move BEFORE school starts each fall. However, the decline in this year was much smaller, and the dollar volume of activity high was an all-time best for September at 14% higher than September 2013 (6% higher transaction volume, 8% higher average sale price). Even more impressive, September 2014 dollar volume was 48% higher than September 2012, which had itself set the record for all-time best Se ptember just 2 years ago.

ptember just 2 years ago.

Saturday, October 4, 2014

Being a real estate agent is actually quite a dangerous job...find out more

There are true dangers of being a real estate agent. The excessive driving, the dangers of meeting up with a roughian and the ability to turn a simple mistake (on a contract) into something that can impact a client's finaincail well being (lawsuit) is always something to consider before jumping into the real estate industry. Real estate is also one of the most costly businesses you will ever run. Find out more by clicking on this ABC News Story

Thursday, October 2, 2014

Zillow Trulia Merger-What it means for you. Does the information get better?

|

|

![]()

![]()

|

Zillow Trulia Merger-What it means for you. Does the information get better?

|

|

![]()

![]()

|

Saturday, September 27, 2014

Thieves use Zillow to con unsuspecting buyers and renters, hear about this need to know info

About four months ago, I got a call from a renter who was asking when he could move into a house that I had listed and sold in Plano Texas. I didn't quite understand what he was asking as I had sold the house and it was never for rent. He had responded to an online Zillow add that showed my listing. Some con-man had copied my listings information and said the house was for rent. The prospective tenant was told to mail the $1200 deposit to an out of town landlord. Needless to say, the out of town landlord was a hoax and the guy on the phone had lost $1200. Anyone can get a Zillow account and start posting anything they want on Zillow. This is also true of many many other websites including Trulia, Craigslist etc. If you really want to be protected when you need a home, you need to be calling a Realtor.

Saturday, August 9, 2014

10 Comandments when applying for a mortgage #buyhousefails

THE TEN COMMANDMENTS

When Applying for a Mortgage

1. Thou shalt not change jobs, become self-employed or quit your job.

2. Thou shalt not buy a car, truck or van (or you may be living in it)!!

3. Thou shalt not use credit cards excessively or let current accounts fall behind.

4. Thou shalt not spend money you have set aside for closing.

5. Thou shalt not omit debts or liabilities from your loan application.

6. Thou shalt not buy furniture.

7. Thou shalt not have any new inquiries into your credit.

8. Thou shalt not make large deposits without checking with your loan officer.

9. Thou shalt not change bank accounts.

10. Thou shalt not co-sign a loan for anyone.

Thursday, August 7, 2014

Keep your home safe while on vacation with these steps

9 Ways to Safeguard Your House Before a Vacation

http://www.bobvila.com/mow-the-lawn/47767-9-ways-to-safeguard-your-house-before-a-vacation/slideshows

http://www.bobvila.com/mow-the-lawn/47767-9-ways-to-safeguard-your-house-before-a-vacation/slideshows

Monday, December 2, 2013

Make sure the agent you hire has your home sale as their priority.

With the rebound of the housing market, home builders are back to building in good and steady volume. What does that mean for the home seller who has to sell their home with a home builder who is still in the neighborhood? It means you are competing against a VERY BIG competitor. You need to sell your home. They need to sell their homes. What they can do that you can't do is they offer HUGE bonuses. $5,000, $10,000, trips, cars...and that's in addition to the typical 3% the agent will make on bringing the builder a buyer.

Builders give bonuses because they know agents specialize in finding buyers. One way we find buyers is our real estate signs. We get sign calls. When you list your home, will place a sign out and put your home all over the internet. When home buyers call about your property your agent has a duty to try and sell your home first. Sometimes, however, the call of those bonuses can be quite alluring. There are many good hardworking agents that want to help you accomplish your goals when you list with them. You need to sell YOUR home not have your house used as a call capture system for an agent who may be steering folks to new construction. For more information or to list your home with an agent that is totally committed to your objectives, call 214-837-0010.

Monday, October 28, 2013

Realtor open house

I'm inviting all real estate professionals to come to my progressive, realtor lunch this Friday at 11:30 a.m. There will be gift cards and lunch provided. Call me at 214-837-0010 to learn more about this even.

Your home failed to sell, now what?

It happens. You put your house on the market and it doesn't sell. Look back and be real honest with your self. Did you insist your agent over price the property when they tried to get you to price it according to market value? Watch the video about pricing your home to sell at www.FreeREVideos.com and learn why you are only hurting yourself by overpricing your property.

Thursday, October 17, 2013

Friday, October 11, 2013

Melissa Texas New Home Construction

The rebound in the housing market has brought new construction back to the forefront in Melissa Texas. In the Liberty subdivision, Highland Homes has come back into the market. Standard Pacific has never left but Khovnanian Homes has take the place of Drees. Longer but narrower lots are part of the new phases. Also, Stonehollow homes continues to be one of the favorite home builder based on what you can get for your money. Their number one seller continues to be NEW homes on larger one acre lots. Look all around Collin and Dallas county. This type of new on an acre property sells starting for $400k. Stonehollow is selling at $230k and up. This is a GREAT deal. Call me and I can give you more info.

Subscribe to:

Posts (Atom)